Success Story: How Debt Consolidation Changed These 4 People’s Lives

Success Story: How Debt Consolidation Changed These 4 People’s Lives

Debt consolidation is the process of combining multiple debts into a single, more manageable loan.

Debt consolidation is a strategy for individuals with credit card debt. Multiple debts are combined into one debt, which is then repaid monthly through a consolidation loan. Debt consolidation lowers your monthly payments and the interest rate on your debt. Additionally, this debt relief solution resolves the monthly confusion for consumers, helping them manage multiple bills and repayment periods from various credit card providers.

A debt consolidation program helps you pay off your unsecured bills through an easy and single monthly payment plan. This program enables you to make only one payment instead of 7 or 8 each month.

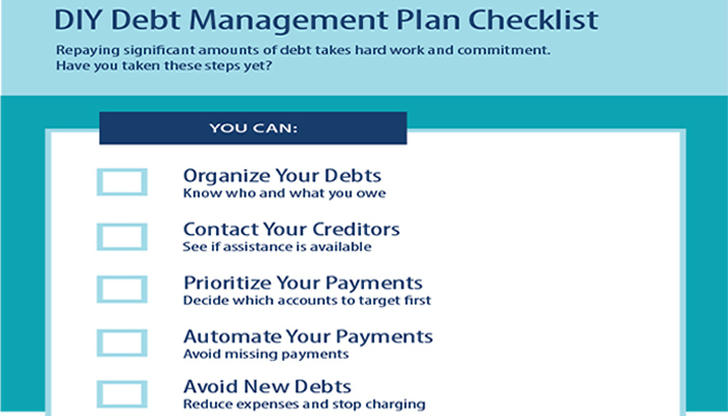

Starting debt consolidation planning early is vital for several reasons:

Avoiding Higher Interest Costs:

Delays could result in more interest on existing debts.

Preventing Debt Accumulation

Without a consolidation plan, individuals might continue to accumulate more debt, worsening their financial situation. For example, ongoing use of credit cards without addressing existing debt can lead to a cycle of increasing balances and interest.

Reducing Stress and Financial Strain

Early planning enables a structured approach to managing debt, reducing the stress and financial strain associated with disorganized payments and missed deadlines.

Improving Credit Score Sooner:

Timely consolidation can enhance credit scores more quickly by lowering credit utilization ratios and avoiding late payments. Waiting too long can delay this positive impact.

Avoiding Collection Actions:

Procrastination might result in missed payments, leading to collection actions or legal issues. Early planning helps in maintaining consistent payments and avoiding such consequences.

Certainly! Here are some illustrative credit card balance transfer success stories based on financial blogs and debt management forums:

1. Jessica’s Balance Transfer Success

Background:

Jessica, a 29-year-old marketing manager, was overwhelmed by $15,000 in high-interest credit card debt. The interest rates made it difficult to reduce her balance significantly, and she felt trapped by mounting interest payments.

Solution:

Jessica decided to transfer her balance to a credit card offering a 0% APR for 12 months with a 3% transfer fee. This move halted interest accrual, allowing her to focus on paying down the principal without additional interest costs.

Outcome:

By the end of the 12-month period, Jessica had fully paid off her $15,000 debt. The balance transfer saved her over $2,000 in interest and improved her credit score, providing her with a fresh financial start.

2. Michael and Sarah’s Consolidation Loan

Background:

Michael and Sarah, a married couple, were struggling with $25,000 in combined credit card and medical debt. Multiple high-interest payments were straining their finances and adding stress.

Solution:

They consolidated their debt into a single lower-interest loan from their credit union. This loan combined their debts into one monthly payment with a reduced interest rate, simplifying their financial management.

Outcome:

The consolidation loan allowed them to manage their debt more effectively, with lower monthly payments and reduced interest costs. They paid off the loan within the term, alleviating financial stress and enabling them to begin saving for their children’s education.

3. David’s Home Equity Loan

Background:

David, a small business owner, was burdened with $30,000 in business debt and $10,000 in personal credit card debt. High-interest rates and multiple payments were straining both his personal and business finances.

Solution:

David used a home equity loan to consolidate both his business and personal debts. This loan offered a lower interest rate and a single monthly payment, significantly easing his financial management.

Outcome:

The consolidation improved David’s cash flow and simplified his finances. He paid off his high-interest debts faster, boosted his credit score, and could focus on growing his business without the stress of multiple debt obligations.

4. Laura’s Dual Consolidation

Background:

Laura, a recent college graduate, was struggling with $20,000 in student loans and $8,000 in credit card debt. Managing both types of debt was overwhelming, and high-interest rates were impeding her progress.

Solution:

Laura consolidated her student loans through a federal Direct Consolidation Loan, which simplified her payments into a single monthly amount with a lower interest rate. She also transferred her $8,000 credit card debt to a balance transfer credit card with a 0% APR for 18 months.

Outcome:

The dual consolidation strategy allowed Laura to manage her student loan payments more easily while eliminating her credit card debt interest-free. By paying off the credit card balance before the promotional period ended, she saved significantly on interest and improved her overall financial stability.

Best Tax Reduction Services August 2024

You don’t have to deal with tax debt alone. Whether you’re dealing with tax collections, payroll deductions, or simply need to update your taxes at a milestone like getting married, buying a home, or managing an estate, we’re here to help. Discover the best tax reduction options for your needs.